Subscribe to join thousands of other ecommerce experts

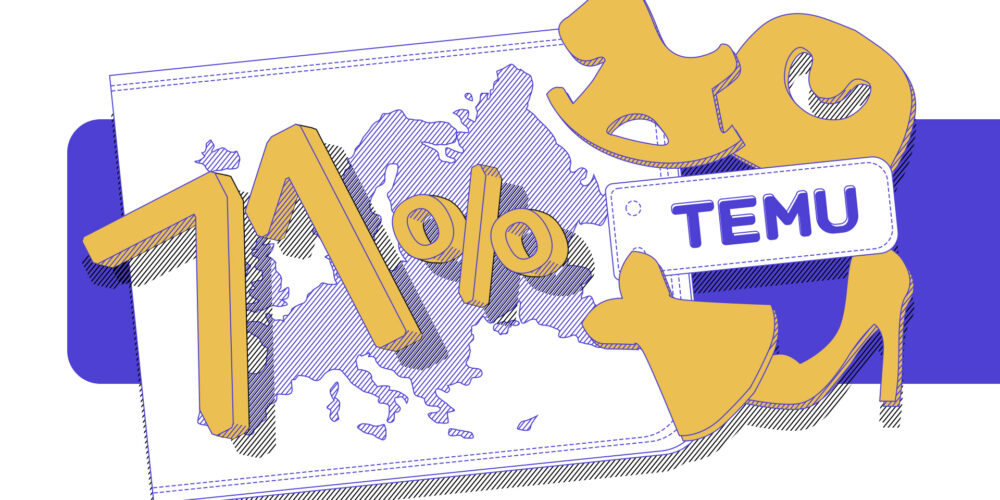

Chinese retail giants are aggressively buying up the European SERP, subsidizing their acquisition costs, and leaving your campaigns to foot the bill. Temu has already captured up to 71% market share in key regions, while JD.com's new contender, Joybuy, is aggressively targeting premium buyers with localized warehouses and same-day delivery.

The result? A massive 23% surge in Standard Shopping CPCs during Q1/2026. This article breaks down the exact data behind this CPC crisis and provides a strategic playbook to outsmart the algorithm, regain control of your margins, and track these giants in real-time.

Remember the “good old days” when your biggest concern was “just” Amazon?

You are no longer competing against the shop down the street. You are fighting an uneven battle against well-funded, government subsidized global players playing by an entirely different set of rules.

It’s no longer just Aliexpress. Major Chinese marketplaces like TEMU, SHEIN and the newest competitor, JD.com’s Joybuy, are aggressively subsidizing their customer acquisition costs, and your campaigns are footing the bill.

Let’s break down exactly what you are up against, starting with the giant that just rewrote the rules of European ecommerce.

Table of Contents

Did Temu just take over Europe?

Temu didn’t just enter Europe: They fundamentally rewired consumer behavior.

To get a better picture as to what Temu’s current market share across the EU looks like, smec’s Head of Ecommerce Insights, Mike Ryan, looked at Temu’s official monthly user stats (as acquired by the European Commission) and then divided them by the number of total active ecommerce users as provided by Eurostat.

Overall, Temu has already captured a staggering 40% market share across Europe. But when you break it down by country, the numbers become even more concerning for Europe’s online shops:

- Italy: A massive 59% market share.

- Germany: 44% market share (Currently their largest single European market by volume).

- France: 42% market share.

- Spain: 49% market share.

But Temu’s real proving ground is the situation in Eastern Europe:

- In Poland, Temu effectively swallowed the market whole, hitting an unprecedented 71.1% market share peak.

- Temu’s effectively dwarfing Poland’s homegrown retail giant Allegro.

There are several strategic implications for your Google Ads campaigns to consider:

- Temu’s market saturation is a direct tax on your company’s growth.

- Incrementality is wildly expensive: The baseline cost to acquire a net-new customer has permanently shifted because these players are buying up the SERP.

- ROAS is blinding you: If your Paid Search team is still treating their advertising budget like an isolated sandbox – optimizing for an arbitrary ROAS target instead of true incremental margin – you are bleeding money.

And if you think figuring out how to compete with Temu’s market saturation is your biggest headache this quarter, brace yourself.

Is Joybuy the new Temu?

Just when you thought you only had to outbid one giant, JD.com stepped into the ring. And they are playing a completely different game.

They recently launched their direct Temu-competitor, Joybuy, across six European markets. But let’s get one thing straight: Joybuy is purposefully not going the Temu route of flooding the market with cheap knockoffs.

Instead, they are walking a highly dangerous sweet spot right between Temu and Amazon. They are pairing Temu-level acquisition budgets with Amazon-level brand quality and fulfillment speed.

Here is why this should concern you:

- Aggressive auction entry: Joybuy is bidding fiercely on the exact bottom-of-funnel clicks domestic retailers rely on. They will happily lose money on the first click to squeeze you out of the auction.

- The “Anti-Temu” brand strategy: Joybuy is coming directly for Amazon’s premium audience. They have a strong focus on high-quality products from renowned, established brands.

- Localized logistics: Unlike Temu’s direct-from-China shipping model, Joybuy launched with over 60 localized European warehouses.

- Same-day delivery focus: They are systematically neutralizing the Western retailer’s biggest historical advantage: fulfillment speed and reliability.

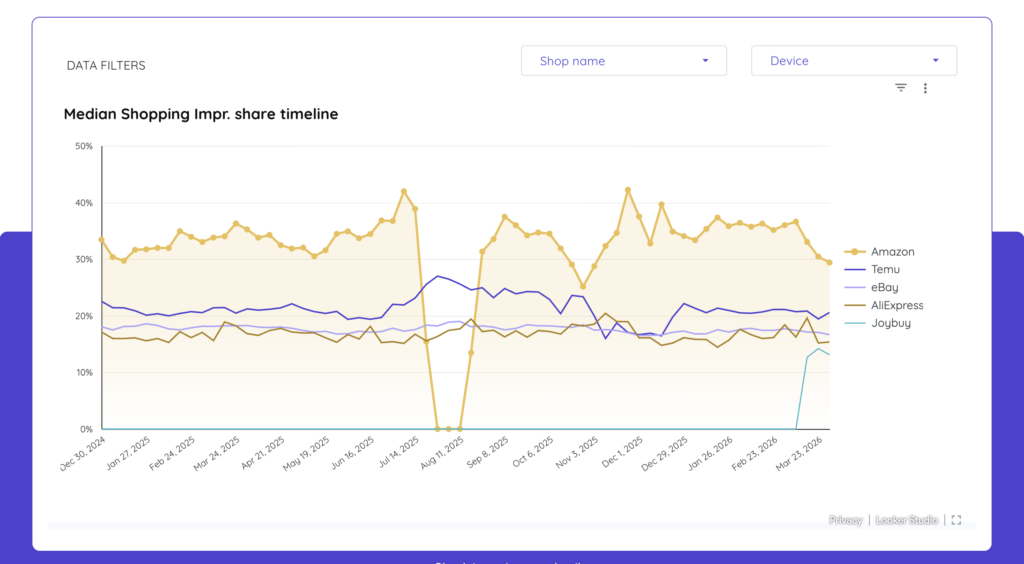

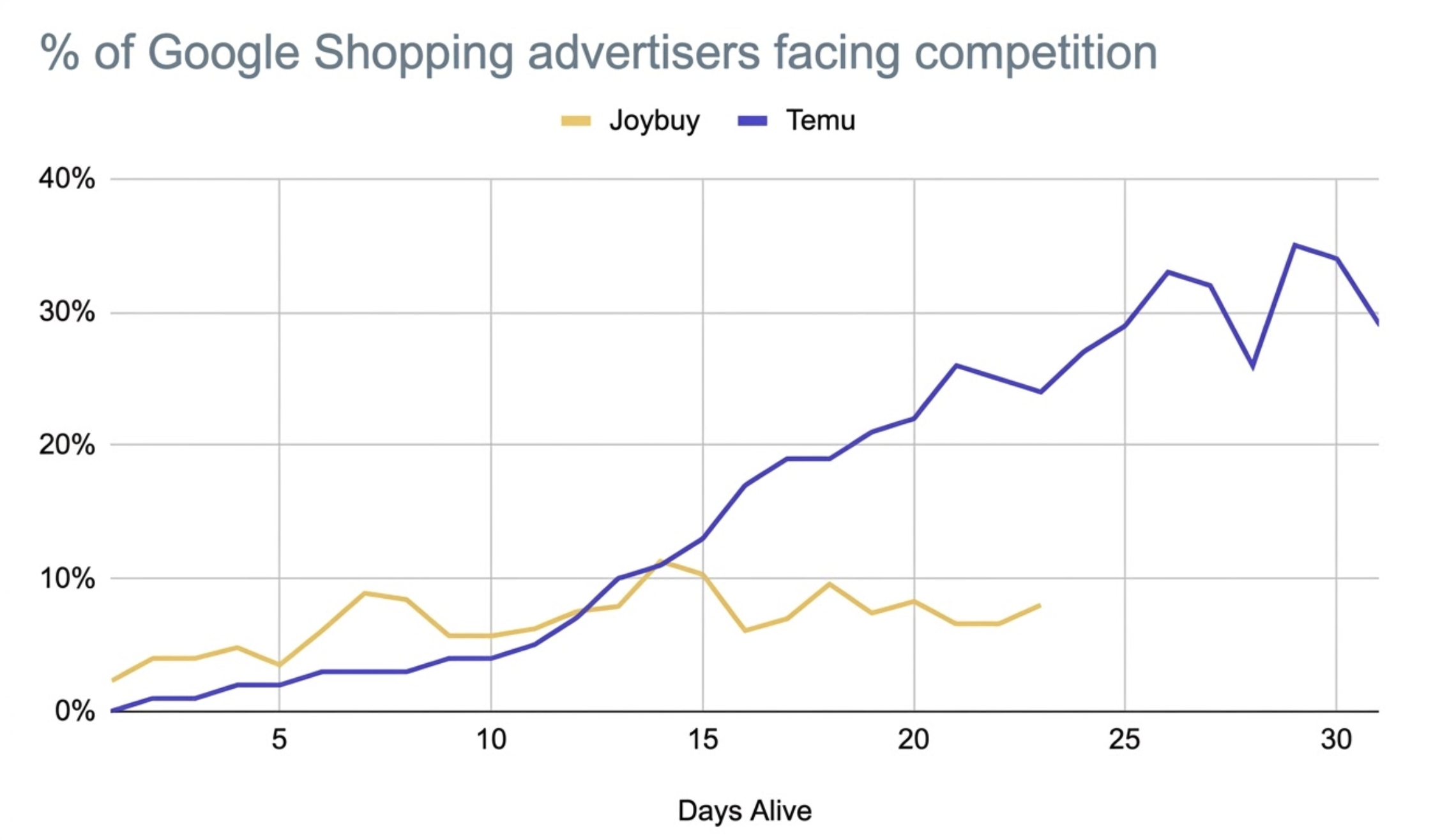

To see if we have a Temu 2.0-style market penetration on our hands, we looked at Joybuy’s impression share since its inception and compared it to Temu’s initial rollout.

Here is what the auction data reveals:

- The initial spike: During their first few weeks, Joybuy’s impression share actually spiked higher than Temu’s did at the exact same stage. This hints at a highly aggressive bidding strategy to seize early momentum and bleed competitors dry.

- The tactical retreat: Right now, Joybuy is floating safely around the 9% to 10% impression share mark. They are likely assessing the landscape and gathering data before making any drastic moves.

Make no mistake: JD.com is not new to this game. They are intimately aware of Europe’s competitive landscape. Don’t be surprised to see another massive hike in Shopping Ads impressions sooner rather than later.

And when that happens, you are going to feel it. Because the immediate financial reality of these two giants clashing is happening right inside your Google Ads account.

How do Chinese marketplaces impact your CPCs?

What happens when giants with billion-dollar acquisition budgets enter the auction? The baseline price rises for everyone.

We took a look at Q1’s Google Ads Benchmarks to analyze the latest CPC trends across Google Shopping, PMax, and Search. The squeeze is obvious:

- Shopping (+23% in Q1): The aggressive budget eater. Jumping from €0.30 in January to nearly €0.38 by March, it has almost completely closed the gap with PMax.

- PMax (+7% in Q1): The steady climber. Ending Q1 at €0.38, it saw a moderate upward spike in March.

Why is Standard Shopping inflating by 23%?

Because you are fighting an uneven battle against global online retail giants with sheer unlimited resources to gain and uphold visibility in the Google Ads auctions.

So, if the old strategy of just turning up the dial on PMax and hoping for the best is a guaranteed way to burn cash, what is the actual way forward? It’s time to stop playing Google’s default game and start playing your own.

The Q2 2026 playbook: Outsmart the unbeatable

You cannot outbid them. So you must outsmart them.

Here is how you adapt your strategy for the rest of the year:

- Ruthless feed hygiene: Don’t pay premium prices for unqualified traffic. Basic titles and descriptions are table stakes now. The new battleground is “conversational attributes.” Google’s AI Overviews and Universal Commerce Protocol (UCP) are hungry for deep, semantic data like Q&As and reviews. Ground the AI with your data before your competitors do.

- Break the “Catch-All” PMax Ttap: Are you running the majority of your company revenue through a single PMax campaign? Stop it. Over-consolidation is a massive risk. Segment your products strategically to regain control over your Heroes and Zombies.

- Prioritize LTV: Joybuy will happily lose money on the first click. Shift your focus from initial ROAS to Customer Lifetime Value (CLV) and Contribution Margin. The cost of growth is up; your strategy needs to reflect that reality.

Long story short: The days of easy, automated wins are over, but the game is far from lost if you are willing to take the wheel. Here is what you need to remember:

- The threat is real: Chinese marketplaces own up to 71% of user share in key European markets.

- Clicks are expensive: Shopping CPCs are up 23% as these giants buy up the auction.

- Strategy beats budget: Stop relying on default platform settings. Take back control, optimize your data feed for AI, and focus on true incrementality.

You cannot execute this strategy if you don’t even know what you are up against. You need one final, crucial piece of the puzzle: Unprecedented market insights.

How to track your industry’s Google Ads Benchmarks in real-time (for free)

If you are relying on gut feeling, delayed reporting, or generic advice from your Google rep to navigate this CPC inflation, you are flying blind.

You need to know exactly when and where these retail giants are pushing into your territory.

That is exactly why we built the smec Google Ads Benchmarks. And because we firmly believe JD’s Joybuy is not a fluke, we just updated it.

Joybuy competitive data is now fully integrated and live.

Here is how you use smec’s Google Ads Benchmarks to regain your competitive edge:

- Track the giants: Monitor the real-time impression share of massive marketplaces like Amazon, Temu, SHEIN, and now, Joybuy.

- Filter the noise: Drill down into your specific industry to see the direct impact these competitors have on your CPCs across Google’s ad surfaces.

- Stop guessing: Know instantly if a performance drop is an isolated campaign issue or a market-wide trend you need to adapt to.

With CPCs rising as fast as these Chinese retail giants are expanding, we think data this critical needs to be free.

Stop optimizing in the dark. Check your industry trends now and steer the machine before your margins evaporate.