Subscribe to join thousands of other ecommerce experts

Update — July 21, 2026: The EU’s €3 import levy is now live as of July 1st, and the pullback this article predicted is showing up clearly in the Google Shopping data. See how Temu and AliExpress retreated from the ad auctions once the fee took effect →

What You Need to Know:

Mike Ryan, Head of Ecommerce Insights at Smarter Ecommerce (smec)

- The Crackdown: As of July 1, 2026, a new €3 EU levy on imports under €150 acts as a 10% tariff on typical €30 orders, breaking the low-cost Chinese C2M (Consumer-to-Manufacturer) business model.

- The Pullback: Google Shopping data shows Temu has halved its ad visibility and SHEIN is nearing a total exit to avoid packages getting hit with fees at the border.

- The Opportunity: This mass advertiser retreat opens a massive ad-space vacuum for Western retailers, though Amazon is already moving in with an earlier Prime Day.

Beginning July 1st, 2026, Europe will enforce a new crackdown on de minimis shipments into their shared market, imposing a €3 levy on import parcels valued less than €150. Their target: the deluge of cheap goods unleashed by Chinese warehouses, propagated by marketplaces, gamified by apps, multiplied by algorithms, and perfected by vast economies of scale.

This is only step one. Step two comes in 2028, when the de minimis loophole will be closed entirely. And meanwhile, regulators both in Brussels and in local jurisdictions have issued fines amounting to hundreds of millions of euros against a scathing litany of violations. These range from environmental degradation and product safety hazards to behavioral dark patterns and a systemic failure to filter out illegal goods.

Back in May 2024, Temu was reportedly concerned about US policymakers’ views toward TikTok, considering Europe a softer target. This might have seemed prophetic when the second Trump administration later used muscular executive orders to impose new global tariffs and end de minimis exemptions in incredibly short order. However, as I wrote back then: “I can’t think of a harbor less safe from regulation than Europe.”

The bloc’s consensus-driven policies might be slow compared to the US, but the message to Chinese firms couldn’t be clearer: clean up and pay up, or get out.

So, is this message landing? One of the most interesting leading indicators we can look at is paid visibility on channels like Google Shopping, since advertising is the gasoline powering their acquisition engines, and it signals the willingness and ability of Chinese giants to invest in the market.

For brands and retailers, this has an impact on channel competition. For shareholders, these are some of the single largest advertisers in Alphabet’s portfolio. For policy watchers, this is economic theory playing out in real time.

Table of Contents

The Google Shopping Barometer

Google Shopping has emerged as a primary marketing channel not only for the likes of Temu, SHEIN, and AliExpress, but also hundreds of smaller C2M and drop-shipping operations out of China and East Asia. Moreover, the advertising presence of these advertisers is highly sensitive to market dynamics, as seen when Temu turned off US advertising overnight due to tariff pressures, a story we first reported.

In this case, advertising is necessarily a leading indicator: customs law doesn’t care when an order was placed or when a package ships; it cares when that arrives at the border. To spell that out, Chinese merchants have shopping times ranging in days to weeks. The closer we get to the July 1st enforcement date, the higher the risk that a package will be subject to the new duties.

SHEIN, Temu, AliExpress, and their peers have to stop their ads now or else risk a huge pile-up in fees. Depending on the scenario, those fees could be covered either by the seller at the border, or by the consumer at their own doorstep. Not a great customer experience.

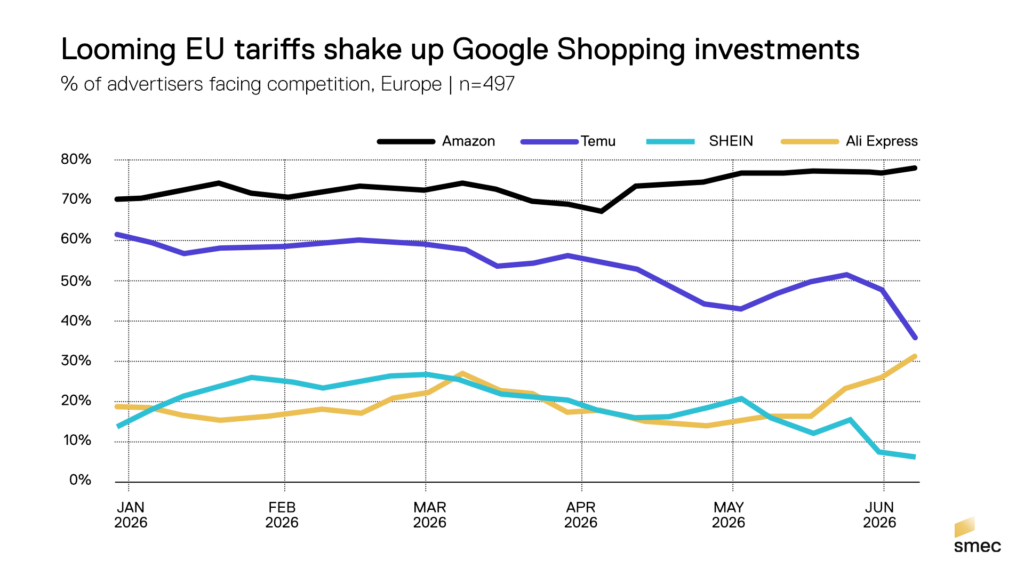

The chart above looks at a sample of about 500 European Google Shopping advertisers, and calculates the percentage that faced account-level competition from these advertisers. Over years of observation, we’ve found this metric is a robust proxy for advertising spend.

What we see here is that Temu and SHEIN started ramping down their ads beginning as early as March 2026. Temu has halved, and SHEIN looks close to exiting the ad auctions altogether. Bewilderingly, AliExpress is actually ramping up their spend and nearing Temu’s level of competition for the first time this year. Perhaps they are trying to squeeze every drop of revenue they can before July 1st, but it’s a dangerous game.

Bear in mind these advertisers are exemplary: there are dozens of smaller merchants likely going through the same budget reductions. For competing merchants looking to soak up any surplus of consumer demand, that’s certainly possible, however Amazon has already been doing exactly that. The timing is not great, since Amazon Prime Day is occurring June 23-26, which is earlier this summer than in years past. Amazon will be peaking their budgets around the same time many of these Chinese advertisers go dark.

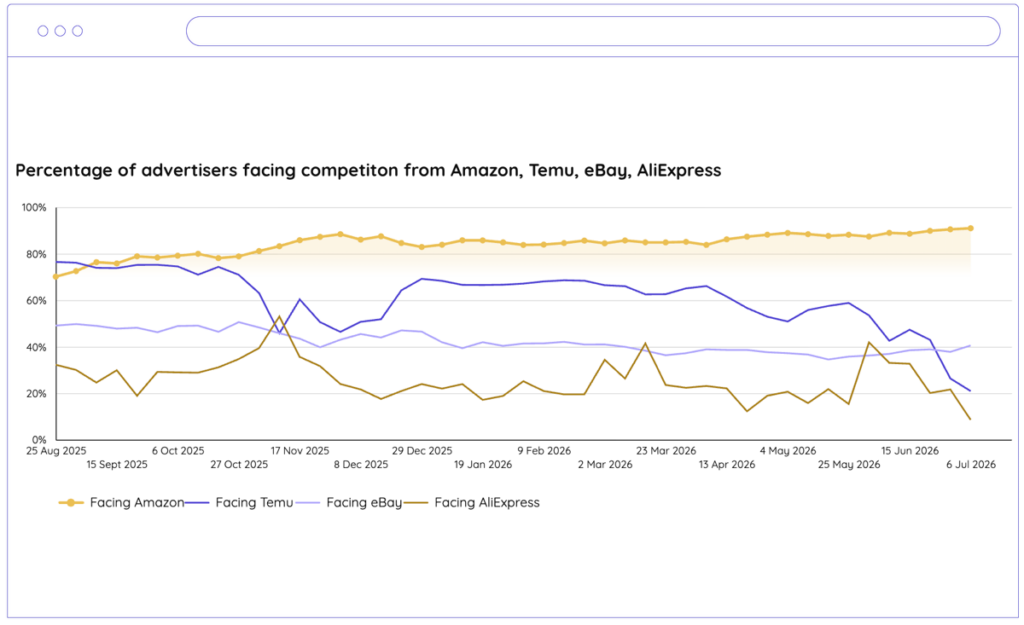

The chart above was the run-up. This next one is the reckoning:

Remember AliExpress — the one player still flooring the accelerator right up to the deadline, squeezing out every last pre-levy order in what I called a dangerous game? The game ended on July 1st. Once the €3 fee went live, AliExpress stopped fighting the current and followed Temu down. The pre-tariff bravado gave way to the same retreat, just a few weeks later.

Turns out nobody wants to be the last advertiser holding a pile of border fees.

We weren’t the only ones watching this play out. In July, Reuters cited our analysis of Google advertiser auction data as independent confirmation that major Chinese advertisers had pulled back their European ad spend once the new fees took effect.

You can follow along with this data as it unfolds at smec Market Observer.

Tariffs are changing the rules.

Competitors are changing their budgets.

Competitors are changing their budgets.

See exactly who is dropping out of the auction

and who is doubling down.

Google Ads Benchmarks

How we got here

While the West has always been an attractive export target for Chinese manufacturers, in the wake of the COVID-19 pandemic this shifted from an expansionary opportunity to a core mandate. This was due to years of so-called involution, a form of domestic stagnation where Chinese firms struggled with the intersection of high competition, high complexity, and high saturation.

Allow me to tell you one of my favorite sayings: “The only way out is through.” To me it signifies toughness and resolve in the face of adversity. However, for Chinese businesses facing a post-pandemic slowdown in an involuted home market, the only way through was out.

And there was indeed a way out.

The C2M model, or reverse-manufacturing model, connects Western shoppers directly to thousands upon thousands of factories in the industrialized deltas of the Pearl and Yangtze rivers. In so doing, nearly every Western middleman is excluded, unlocking cost savings. Instead of pocketing these, the savings are transferred toward end consumers in the form of unbeatable prices, which in turn attracts market share.

While there are many dimensions of C2M we could look at, three are most relevant today:

- Ecommerce: This is the interface to consumers, the digital shelf. Chinese sellers have become central to Amazon’s legendary “flywheel.” But why should Amazon own that?

- De minimis exemptions: This is the golden tickelent, the asymmetrical advantage that allows Chinese platforms like Temu and SHEIN to completely bypass import taxes on small shipments.

- Ads: This is the gasoline. Google Shopping ads function largely as a price comparison tool, which plays to the C2M model’s strengths. And if you want to spend billions there, no one is going to stop you.

How the new tariffs work

If a €3 fee sounds trivial, consider its effect at scale on the landed cost of Chinese merchants. €30 is the approximate average order value of companies like Temu, which means that a €3 fee is already equivalent, on average, to a 10% tariff. Furthermore, this fee is not applied per parcel, but rather per customs declaration line per parcel. In other words, a Temu package containing one dress, one cellphone case, and one USB charger could see up to €9 in fees.

Although Europe couldn’t defend its market as quickly as the US, and although the full closure of the de minimis loophole cannot be completed until digital infrastructure is prepared in 2028, their solution is nevertheless robust.

€3 is all it takes to break these business models in many categories, and bulk import is already more attractive than an unpredictable hodgepodge of per-parcel tariffs.

The only question: having been chased from the US, and now, it seems, from Europe, where will all those big orange boxes go next?

Amazon will be peaking their budgets around the same time many of these Chinese advertisers go dark.

However, fortune favors the bold. For advertisers looking to gain market share, July presents a rare opportunity in the post-Prime Day vacuum, expected to be largely devoid of many non-EU advertisers. They can do so by increasing budgets and relaxing efficiency targets, particularly in categories where these advertisers were previously dominant.

Ready to capture the vacant ad space?

As Chinese ecommerce giants pull back from Google Shopping auctions, a massive window of opportunity is opening up for Western brands. But you won’t be the only one trying to seize it. To win this shifting market, you need advanced automation and battle-tested expertise. At smec, we combine 18 years of specialized ecommerce experience with a scalable Google Ads management platform built to out-compete the market.

source on Google →